Every trip has two budgets. The one you plan. And the one that quietly leaks away in fees, bad exchange rates and sneaky card tricks.

If you’ve ever come home and thought, How did I spend that much?

there’s a good chance some of that money went to Dynamic Currency Conversion (DCC), aggressive ATM fees, and card charges you never meant to accept.

This guide breaks down the main tourist money traps overseas, how they work behind the scenes, and the exact choices to make at terminals and ATMs so more of your cash stays with you, not the banks.

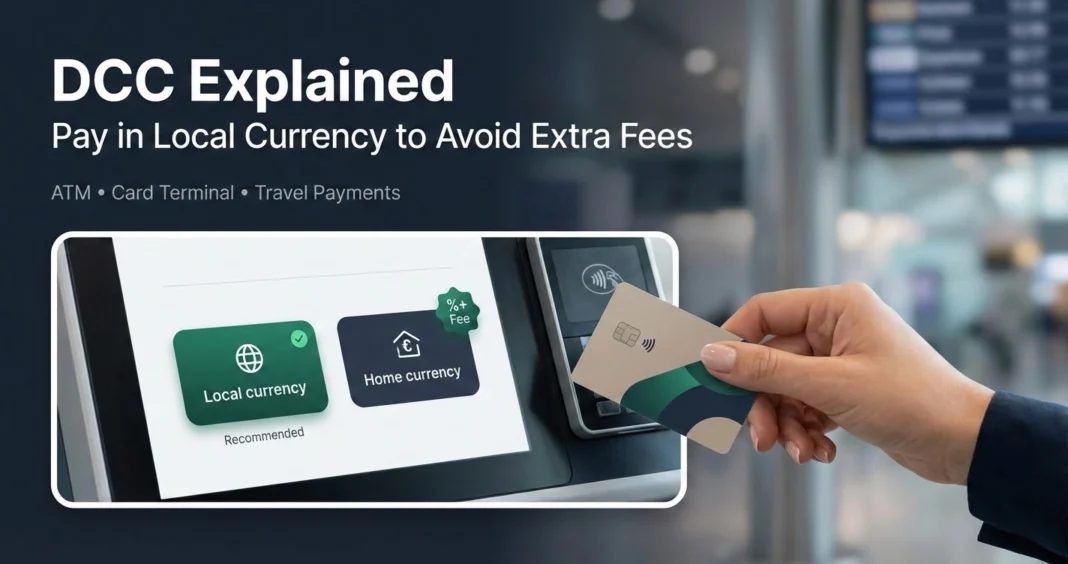

1. The Big One: Dynamic Currency Conversion (DCC) – Why “Pay in Your Currency?” Is a Trick Question

You’re abroad, the card terminal flashes a choice:

- Pay 1,000.00 LOCAL

- Pay 98.50 HOME CURRENCY (guaranteed rate!)

The familiar number in your home currency looks comforting. It feels safe. Clear. Transparent.

But here’s what’s really happening with Dynamic Currency Conversion (DCC) when you’re traveling:

- The merchant’s processor (not your bank) converts the amount into your home currency on the spot.

- They use an exchange rate that’s often 4–8% worse than the real market rate – sometimes even more at ATMs.

- You may still get hit with your bank’s foreign transaction fee on top of that.

So you’re effectively paying twice: once in the hidden markup baked into the rate, and again in your bank’s fee.

In one real example from Italy, a €200 ATM withdrawal with DCC would have cost about $29 more than just taking the local-currency option. Same cash. Same machine. Different button.

My rule: when I see a choice between my home currency and the local one, I always choose local currency. If I can’t decline DCC, I cancel the transaction and walk away.

Quick DCC checklist at the terminal or ATM:

- Look for phrases like

pay in your currency

,guaranteed rate

,dynamic currency conversion

, orwe convert for you

. - Find and select options like

charge in local currency

,continue without conversion

, ordecline conversion

. - If the machine doesn’t let you refuse DCC, cancel and find another.

2. Why Paying in Local Currency Is Almost Always Cheaper

So what happens when you don’t accept DCC and just pay in the local currency?

Then the conversion is handled by your card network and bank instead of the merchant’s processor. That’s a big difference.

- Visa and Mastercard usually use rates very close to the interbank rate – the real market rate banks use with each other.

- Your bank may add a small margin or a foreign transaction fee (often 1–3%), but that’s still usually far less than DCC’s 4–8%+ markup.

- There’s no extra middleman taking a cut just because you pressed the “convenient” button.

In other words, when you choose local currency, you’re letting the system that already handles millions of cross-border payments daily do its job. When you choose DCC, you’re paying a premium for a service you didn’t need.

My setup when I travel:

- Use a credit card with no foreign transaction fees for almost all purchases.

- Always choose local currency on the terminal instead of my home currency.

- Ignore the “guaranteed rate” sales pitch – it’s guaranteed to be better for them, not for me.

If you want to dig into the mechanics, there’s a good overview on DCC and markups on Wikipedia. The practical takeaway for dynamic currency conversion travel decisions is simple: local currency wins almost every time.

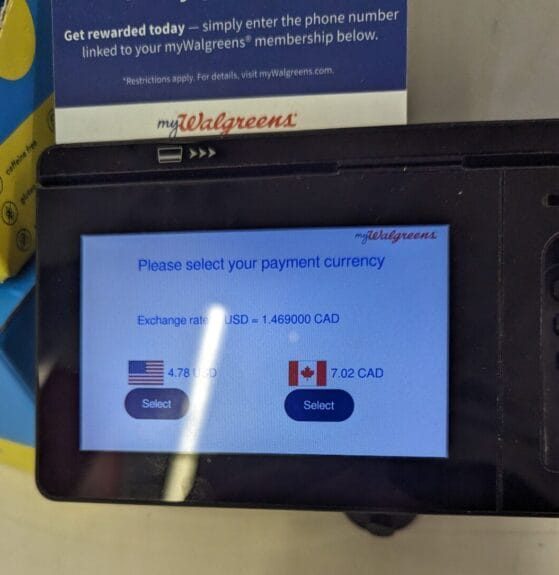

3. ATM Minefield: Fees, DCC and the “Helpful” Warnings That Aren’t

ATMs abroad are where DCC and fees get really nasty, because you can be hit by three layers of cost at once:

- ATM operator fee – a fixed charge per withdrawal (e.g., €3–€7).

- DCC markup – a terrible exchange rate if you choose to see the amount in your home currency.

- Your bank’s own fees – foreign ATM fee + possible foreign transaction fee.

Independent ATMs in tourist zones (airports, busy squares, near attractions) are often the worst offenders. They’re designed to catch tired, rushed travelers who just want cash and will tap through any warning.

Watch for this pattern:

- The ATM shows a scary message like

We strongly recommend our guaranteed conversion to avoid unknown bank fees

. - It highlights the DCC option in big, friendly buttons.

- The

continue without conversion

ordecline

option is small, grey, or worded confusingly.

That warning is not for your benefit. It’s there because the ATM operator earns a cut of the DCC markup.

My ATM rules abroad:

- Prefer bank-branded ATMs attached to real banks, not random machines in shops or hotel lobbies.

- Always choose local currency and look for

continue without conversion

. - If the ATM forces DCC or hides the local-currency option, I cancel and find another.

- Withdraw larger amounts less often to spread any fixed ATM fee over more cash.

- Use a debit card from a bank that reimburses ATM fees or charges minimal foreign ATM fees when possible.

One more subtle trap: some ATMs show you the effective exchange rate they’re offering. If it looks significantly worse than what you see on a quick Google search for USD to EUR

(or whatever pair you’re using), that’s your cue to back out. That’s how you avoid ATM fees abroad turning into a much bigger hit through bad conversion.

4. Card Charges You Don’t See Coming: Foreign Transaction Fees & Hidden Costs

Even if you dodge DCC and pick good ATMs, your own card can still quietly drain your budget.

Two main culprits:

- Foreign transaction fees – usually 1–3% of every purchase made abroad or in a foreign currency online.

- Cash advance fees and interest – when you use a credit card at an ATM instead of a debit card.

Here’s the twist: even if a transaction is charged in your home currency via DCC, many banks still treat it as a foreign transaction because it happened abroad. So you pay the DCC markup and the foreign transaction fee.

If you’ve ever looked at your statement and wondered why your trip cost more than expected, this is often the reason. Those foreign transaction fees on travel cards add up fast.

My card strategy before a trip:

- Carry at least one credit card with 0% foreign transaction fees.

- Use a debit card (not credit) for cash withdrawals to avoid cash advance fees and immediate interest.

- Check my bank’s ATM fee policy – some refund foreign ATM fees up to a limit.

And I always assume:

- If a terminal or ATM is pushing DCC, it’s not doing it to save me money.

- If my bank charges foreign transaction fees, every overseas purchase is a little more expensive than it looks.

That’s why combining no-foreign-fee cards with local-currency payments is such a powerful combo. You remove both the obvious and the hidden markups and avoid the worst credit card traps for tourists.

5. When (If Ever) Saying Yes to DCC Might Make Sense

Is DCC always bad? Almost. But there are a few edge cases where someone might accept it knowingly and still sleep at night.

Possible exceptions:

- You’re making a very small purchase and you truly don’t care about losing a few cents for the comfort of seeing your home currency.

- Your bank charges an unusually high foreign transaction fee and you’ve done the math (carefully) and know DCC is somehow cheaper in that specific case.

- You need a fixed, known amount in your home currency for strict expense reporting, and your employer doesn’t care about the extra cost.

Even then, I’d still ask myself:

- Is the convenience worth paying 4–8% more?

- Could I get the same clarity by checking my card’s exchange rate later in the app or statement?

For almost all travelers, almost all of the time, the answer to pay in local currency or home currency?

is simple: decline DCC, pay in local currency, and keep that extra percentage for yourself.

6. Quick Decision Guide: What to Do in Real-Life Situations

Let’s turn this into a simple playbook you can run on autopilot. Think of it as your pocket-sized travel money cost guide.

At a restaurant or shop abroad

- Terminal asks:

Pay in HOME CURRENCY or LOCAL CURRENCY?

- Choose: LOCAL CURRENCY.

- If staff insist on your home currency, politely ask them to rerun it in local currency or write the amount and dispute later if needed.

At an ATM abroad

- Screen shows a

guaranteed rate

in your home currency. - Look for

continue without conversion

,decline conversion

, orcharge in local currency

. - If you can’t find it, cancel and try another ATM, ideally at a bank branch.

Booking hotels, tours or tickets online in foreign countries

- Website offers to charge you in your home currency.

- Choose the original local currency of the merchant.

- Pay with a card that has no foreign transaction fees.

Before your trip

- Check which of your cards have 0% foreign transaction fees.

- Bring at least one backup card from a different bank.

- Know your bank’s ATM fee policy and daily withdrawal limits.

If you remember nothing else about travel money mistakes to avoid, remember this:

Local currency. No DCC. No foreign transaction fees if you can avoid them.

7. Turn the Tables: Keep the Rewards, Skip the Traps

Travel doesn’t have to be a game where the house always wins. The same card that gets you into airport lounges or earns you points can also quietly bleed money if you don’t control how it’s used abroad.

So next time you’re at a terminal or ATM and see that friendly offer to pay in your currency

, pause for half a second and ask yourself:

Who actually benefits if I say yes?

Most of the time, it’s not you.

Say no to DCC, yes to local currency, and let your money fund more of your trip instead of someone else’s margins. That’s how you sidestep the worst hidden travel money charges, keep debit card charges when traveling under control, and make sure your overseas card fees breakdown looks a lot less painful when you get home.