I used to think about travel health costs in simple terms: How much is a doctor visit in X country?

Then I started seeing real bills. Not listicles. Actual invoices from travelers who got sick or injured abroad.

That’s when the question changed for me. The real issue isn’t the price of a quick checkup. It’s this: What’s the worst-case bill if everything goes wrong? Because when you’re in a foreign ER at 2 a.m., you’re not comparing local clinic prices for tourists. You’re just trying not to die.

In this guide, we’ll walk through the hidden costs of getting sick abroad, region by region, and compare the three paths most travelers end up on:

- Self-pay – you pay cash, no insurance

- Local clinics and hospitals – with or without insurance

- Medical evacuation – when you need to be flown out

The goal isn’t to scare you. It’s to give you enough detail that you can look at your next trip and think, Okay, if this goes sideways, I know roughly what I’m on the hook for.

That’s how you avoid nasty surprises with out of pocket medical expenses abroad.

1. The First Decision: Are You a Tourist, a Nomad, or Something in Between?

Before we talk numbers, you need to know which healthcare bucket you fall into. The same hospital can charge wildly different prices depending on who you are and how you’re classified.

Most travelers I meet fall into one of three groups:

- Short-term tourists – usually covered by travel insurance (if they bought it) and treated as private patients abroad.

- Digital nomads / long-stay travelers – often in a gray zone: not residents, not tourists, and frequently under-insured.

- Expats / residents – may have access to public systems or employer insurance, but still use private care for speed or language.

Here’s the uncomfortable part: visa status matters more than country reputation. A country can have universal healthcare and still charge you full private rates if you’re on a tourist or digital nomad visa. That’s where a lot of uninsured traveler medical costs come from.

As Nomad Wallets points out, nomads often get pushed into the private tier even in countries with public systems. That $20–$30 doctor visit you saw on a blog? That’s often the headline price. Add labs, imaging, and prescriptions and you’re suddenly in the hundreds. That’s how the hidden costs of getting sick abroad sneak up on people.

So the first decision is simple, but not always pleasant:

- Are you planning as a tourist – short stay, insured, in-and-out?

- Or as a temporary resident – gray zone, often self-pay, maybe partial access to public care?

If you’re in that gray zone, assume private-tier pricing and plan accordingly. Think of yourself as a private patient, not a local.

2. The Self-Pay Trap: When “Cheap” Countries Aren’t Cheap Anymore

There’s a seductive myth that floats around travel forums: Healthcare is cheap abroad.

Sometimes it is. Often it isn’t. And when it isn’t, it’s usually because you’ve crossed an invisible line from a simple visit to a full medical event.

Here’s what data from Jetset Protect and other sources shows about self pay medical costs overseas:

- Even in “affordable” countries, a serious emergency (ER + surgery + multi-night stay) can easily hit $20,000–$30,000.

- Nearly half of uninsured American travelers who needed care abroad came home with $20,000+ in medical debt.

- Medical inflation in Asia and Latin America is rising faster than general inflation, so

2022 prices

are already outdated.

And that’s before we even talk about medical evacuation cost by region.

One of the best reality checks I’ve seen is a real case: appendicitis abroad with ICU and evacuation. Total bill: $166,100. A typical $50,000 policy would have left over $100,000 unpaid. A $250,000 policy? Fully covered.

On the other side of the spectrum, there’s the early retiree who broke her wrist in Thailand, then chose to have it treated at a private hospital in Kuala Lumpur. She skipped insurance entirely and paid about $1,450 for a mid-range treatment option at Gleneagles Hospital. That fit within her $2,000/month travel budget. It worked—this time.

So where’s the trap?

- You hear a few success stories about cheap care abroad.

- You assume,

Self-pay is fine, I’ll just go to a private hospital if needed.

- You forget that one bad roll of the dice can turn a $1,450 story into a $50,000+ story.

Self-pay can work if:

- You have a real emergency fund (not just a credit card).

- You’re comfortable making medical decisions based on cost vs function (like choosing 80–90% wrist function instead of 95% because surgery is too expensive).

- You’re okay with no safety net if the situation escalates.

If that last point makes you uneasy, you’re not alone. That’s usually the moment people start looking at a travel medical cost comparison and rethinking their plan.

3. Region by Region: What Self-Pay Really Looks Like

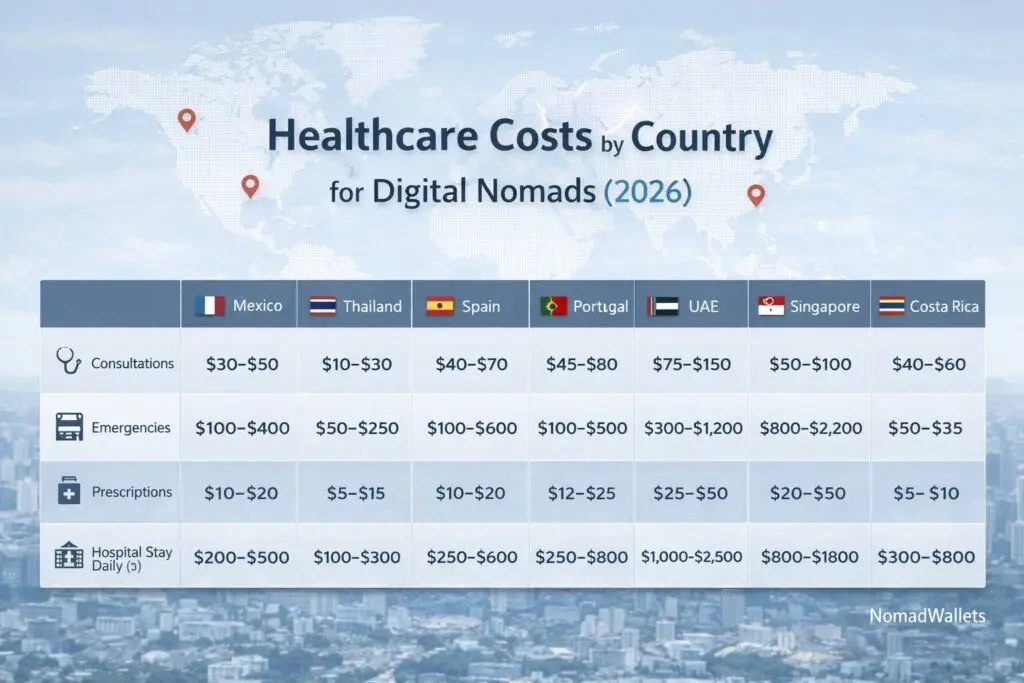

Let’s zoom out and look at how self-pay and out of pocket medical expenses abroad stack up by region. These are broad ranges, but they’re grounded in real-world data and actual international medical bills for travelers.

North America & the Caribbean

- United States: Among the most expensive in the world. An overnight hospital stay can average around £7,000 (roughly $8,000–$9,000). A moderate emergency can easily hit $20,000+.

- Caribbean: Many islands rely on private hospitals. Serious cases often get transferred to the U.S., which means you’re paying both local and U.S. rates, plus possible evacuation.

If you’re uninsured and traveling in this region, you’re essentially gambling with U.S.-level pricing. The cost of emergency treatment overseas here can be brutal.

Europe

- Public systems (e.g., UK, Portugal, Spain) can be relatively low-cost, especially if you’re a legal resident or have reciprocal agreements.

- Tourists often still pay for doctor visits, prescriptions, and ambulances, even with EHIC/GHIC or similar cards.

- Private hospitals in places like Switzerland can approach or exceed U.S. prices.

Europe is where many travelers get lulled into complacency: They have universal healthcare, I’ll be fine.

Maybe. But if you’re not in the system, you’re often treated as a private patient. That’s one of the classic mistakes with medical bills overseas.

Asia

This is where the story gets more nuanced, and where regional differences in healthcare costs abroad really show up.

- Thailand & Malaysia: Strong private sectors, many JCI-accredited hospitals, and costs up to 75% cheaper than Western countries for many procedures. But private care is still real money—surgery and multi-night stays can easily exceed £10,000.

- Singapore: High quality, but private care can approach U.S. pricing.

- South Korea & Taiwan: Fantastic value if you’re in the national insurance systems. For residents, doctor visits can be $5–$20. For tourists? Expect private-tier pricing.

Asia is where many digital nomads decide to self-insure because the average

costs look low. But remember: you don’t budget for the average. You budget for the outlier—the one big event that blows up your travel health cost breakdown.

Latin America

- Mexico, Colombia, Costa Rica, Brazil: Public systems can be very affordable or even free for residents. Private care is still cheaper than the U.S., but not trivial.

- Digital nomads and tourists often end up in private clinics, especially in big cities and tourist hubs.

One traveler I spoke with paid a tiny fee for a clinic visit in Mexico—great story. But that same system can still produce four-figure bills for surgeries and hospital stays, even at cheap

rates. The hidden costs of getting sick abroad show up fast once you move beyond basic care.

Bottom line

Self-pay can be manageable for minor issues. Once you cross into surgery, ICU, or multi-night stays, the numbers jump fast—almost everywhere. That’s true whether you’re in a budget destination or a high-cost country.

4. Local Clinics vs Big Hospitals: Which Door You Walk Through Matters

When something goes wrong abroad, you often face a split-second decision: small clinic or big hospital? That choice can change your bill by thousands.

Here’s how to think about it when you’re weighing self pay vs local clinic vs medevac.

Local clinics (and small private hospitals)

Pros:

- Lower consultation fees (often $20–$50 in Southeast Asia, similar in parts of Latin America).

- Faster access, less bureaucracy.

- Good for minor issues: infections, small injuries, basic diagnostics.

Cons:

- Limited diagnostics (may need to send you elsewhere for imaging or complex labs).

- May not be equipped for surgery, ICU, or complex emergencies.

- Quality can vary widely; you need to vet them or get recommendations.

Large private or international hospitals

Pros:

- Full diagnostics on-site (CT, MRI, advanced labs).

- Specialists and surgeons available.

- Often more accustomed to foreign patients, English-speaking staff, and insurance billing.

Cons:

- Higher base prices: GP visits can be $60–$90 or more in Southeast Asia, higher in Europe and Singapore.

- Everything is itemized: bed fees, nursing, medications, supplies—costs add up fast.

- They may require upfront payment or proof of insurance before major procedures.

Remember the wrist fracture story in Kuala Lumpur? The traveler had three options:

- Surgery with plate and screws (plus a second surgery later): $4,600–$8,600.

- Closed reduction under general anesthesia with live X-ray and casting: $1,150–$2,700.

- Simple cast without resetting the bone: much cheaper, but worse long-term function.

She chose option 2 and paid about $1,450. That’s the kind of decision you make when you’re self-pay: constantly balancing cost, function, and future uncertainty.

So how do you choose in the moment?

- Life-threatening or severe trauma? Go to the best-equipped hospital you can reach. Money is secondary.

- Moderate but stable issue? Start with a reputable clinic or smaller private hospital, especially if you’re self-pay.

- Minor issue? Consider telehealth or walk-in clinics (even retail clinics in the U.S. like CVS or Walgreens) to keep costs down.

The key is to decide before you travel which door you’re likely to choose—and how you’ll pay for it. That’s where a clear travel health cost breakdown helps.

5. The Nuclear Option: Medical Evacuation and Why $50,000 Isn’t Enough

This is the part most travelers don’t want to think about: what happens if you need to be flown out?

Medical evacuation is where the numbers go from painful

to catastrophic. It’s the line item that turns a big bill into a life-altering one.

Based on data from Jetset Protect and similar sources, here’s what a medical evacuation pricing guide looks like in real life:

- Many medical evacuations cost $100,000–$250,000+.

- Routes from remote regions (Africa, Nepal, South Pacific) to the U.S. can hit $150,000–$300,000, especially if helicopters plus long-range medical jets are involved.

- Even regional evacuations (e.g., from a small island to a major city) can run into the tens of thousands.

Now layer that onto hospital costs. That appendicitis case with ICU and evacuation? Total: $166,100. A $50,000 policy barely made a dent. A $250,000 policy covered it.

This is why I’m skeptical of budget travel insurance with $50,000 medical limits. On paper, it looks fine. It covers most normal

emergencies. But once evacuation enters the picture, that limit can disappear in a single event.

So ask yourself:

- Where am I traveling? How far is it from a major medical hub?

- What’s the realistic worst-case scenario? (Think: trauma, stroke, heart issue, severe infection.)

- Would I want to be evacuated home, or would I be okay being treated locally?

If your honest answer is I’d want to be flown home

, then a $50,000 limit is almost certainly too low. For many routes, it’s not even close.

6. Insurance vs Self-Funding: What Actually Makes Financial Sense?

Let’s strip away the marketing and talk about the math behind self pay vs local clinic vs medevac.

On one side, you have robust travel insurance with medical limits of $250,000 or more, often including evacuation. On the other, you have self-funding with an emergency buffer and maybe a basic policy or none at all.

Here’s what the numbers and case studies suggest:

- A few hundred dollars in premium can offset a low-probability but extremely high-cost risk.

- Travelers with comprehensive policies have walked away from six-figure bills fully covered.

- Uninsured travelers have faced bills like $186,500 and turned to crowdfunding.

So why do people still under-insure?

- They focus on probability (

It probably won’t happen

) instead of impact (If it does, I’m ruined

). - They see $50,000 and think it’s a big number without realizing how fast it disappears once evacuation and ICU are involved.

- They underestimate how often evacuation is needed, especially from remote or developing regions.

Here’s a simple framework:

- If you can’t comfortably write a $100,000 check without wrecking your life, you probably need robust medical + evacuation coverage.

- If you’re a long-term nomad, consider a mix: global health insurance for big stuff + self-pay for routine care. Use local clinic prices for tourists and residents for everyday issues, and keep insurance for the big shocks.

- If you’re an expat with public coverage, check what’s excluded (private rooms, certain drugs, evacuation) and plug those gaps.

Yes, there are edge cases where self-funding makes sense: high net worth travelers, people fully integrated into public systems, or those who consciously accept higher risk. But for most people, under-insuring is a false economy. You save $50–$100 on premiums and take on a six-figure tail risk.

7. Practical Playbooks by Region: What I’d Actually Do

Let’s make this concrete. If I were planning trips or long stays in different regions, here’s how I’d approach the travel medical cost comparison and the self-pay vs clinic vs evacuation question.

Europe (including UK, Portugal, Spain)

- Short trips: Travel insurance with at least $250,000 medical + evacuation. I’d still expect to pay out of pocket for some doctor visits and prescriptions, especially as a tourist.

- Long stays / residency: Get into the public system as soon as possible, then use private clinics for speed. Insurance becomes more about gap coverage and evacuation.

Asia (Thailand, Malaysia, Singapore, Korea, Taiwan)

- Short trips: Same as Europe, but I’d be extra careful with evacuation limits if I’m going somewhere remote (islands, mountains).

- Digital nomad base: Budget for private-tier care. Consider a global health plan if I’m staying 6–12 months or more. Use local clinics for routine issues, big hospitals for serious stuff.

- Residency in Korea/Taiwan: Get into national insurance (NHIS/NHI) and then decide if I need extra private coverage or evacuation add-ons.

Latin America (Mexico, Colombia, Costa Rica, Brazil)

- Short trips: Robust travel insurance, same logic as above.

- Residency: Join public systems (e.g., EPS in Colombia, Caja in Costa Rica, SUS in Brazil) and supplement with private insurance or savings for faster access and better facilities.

North America & Caribbean

- U.S. trips: If I’m not covered by domestic insurance, I treat the U.S. as a high-risk destination and prioritize strong travel medical coverage.

- Caribbean: I assume that serious issues may end up in the U.S. and choose evacuation coverage accordingly.

In all regions, I’d keep a few constants:

- A list of reputable clinics and hospitals near where I’m staying.

- A clear understanding of my policy limits and what triggers evacuation.

- A personal rule: never travel without at least some form of medical + evacuation coverage unless I’m truly prepared to self-fund a worst-case scenario.

8. Your Personal Line in the Sand

At some point, this stops being about averages and case studies and becomes personal. You have to decide where your line in the sand is.

Ask yourself:

- What’s the biggest bill I could realistically absorb?

- Am I okay making medical decisions based on cost? (Choosing a cheaper procedure with worse long-term function, for example.)

- How far from home am I willing to be when something serious happens?

If your honest answers make you uneasy, that’s not a failure. It’s information. It’s a signal to adjust your plan—whether that means buying better insurance, choosing different destinations, or building a bigger emergency fund.

The hidden costs of getting sick abroad aren’t just financial. They’re emotional, logistical, and sometimes moral. But the financial piece is the one you can actually plan for.

You don’t have to obsess over every worst-case scenario. You just have to be clear-eyed enough to say:

If I roll a bad number on this trip, I won’t be ruined.

That’s the real goal. Not zero risk. Just no surprises big enough to break you.